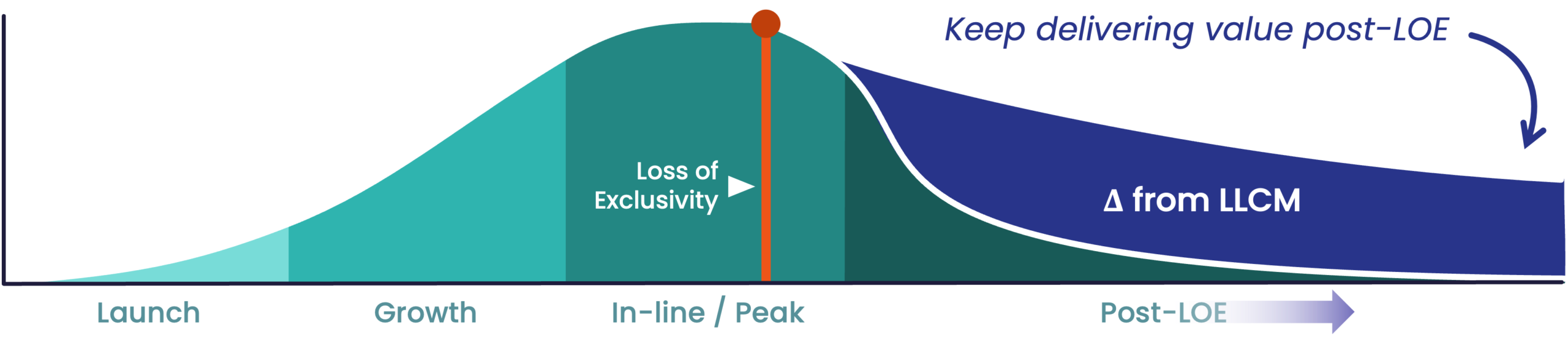

Loss of exclusivity (LOE) is not merely a regulatory milestone – it is a strategic stress test for pharmaceutical brands. While exclusivity offers a period of controlled growth and market leadership, its end exposes brands to rapid commoditization driven by the entry of generics. Navigating patent expiry successfully requires more than defensive tactics; it calls for deliberate late lifecycle management, delivering forward-looking brand evolution that anticipates how local market dynamics will change and where value can still be sustained.

Loss of exclusivity does not create a single, predictable outcome. Instead, it reveals a diverse and fragmented set of local realities that demand nuanced understanding and targeted strategic responses.

For brands aiming to slow their descent from the patent cliff and remain competitive in a reshaped landscape it is critical that team’s move early to:

- Prepare for loss of exclusivity well ahead of patent expiry

- Shift from a global mindset to locally-led decision‑making

- Develop a nuanced understanding of how local markets will diverge post‑LOE

In this article, we focus on the key local dynamics that determine how loss of exclusivity will actually play out in a given market, and what teams need to understand to plan for it effectively.

Shifting The Focus to Local Markets

In early and mid‑lifecycle stages, global brand strategy plays a central role in driving consistency and scale. While local adaptation is always required, market strategies tend to remain rooted in the brand’s unique value proposition, and as such local strategy will have more in common with the global strategy than not.

As loss of exclusivity approaches, this balance fundamentally shifts. Brands need to prepare for an environment where they no longer have sole claim to the molecule’s clinical value proposition. From this point, local dynamics have a much more important baring on the management of the brand as both the source of value erosion and the opportunity for resilience.

We have previously explored the merits of transitioning from a global-led to a locally driven brand planning process as loss of exclusivity approaches. This shift is not about abandoning global direction, but about relocating decision authority to where insight into post‑LOE realities is deepest.

The critical question then becomes: what local dynamics matter most when planning for the late lifecycle?

How Loss of Exclusivity Shapes Key Local Dynamics

Understanding Competition Post-LOE

The first area that needs to be understood when preparing for LOE, is the generic competition that the brand expects to face both in terms of the type of competition (the companies commercializing the generics) and the intensity of that competition.

Competitive intensity (i.e. the number of generic entrants) is a key driver that will shape local dynamics post-LOE. This can often be anticipated by understanding the attractiveness of the opportunity for generic manufacturers, including the commercial potential, product complexity, and local competitive archetype. The resulting intensity directly impacts generic pricing strategies and the likelihood of local pricing controls or procurement intervention.

However, which competitors enter a market matters just as much as how many. Local dynamics differ substantially depending on whether competition comes from:

- Global generics players with scale and portfolio leverage

- Local branded players with HCP/patient trust and heritage

- Local generic players with low cost and deep supply relationships

- Pharmacy‑led white‑label players with a captive patient base.

Each of these competitor types shapes pricing behavior, stakeholder influence, and brand defensibility in different ways.

It is therefore important to have appropriate competitive intelligence monitoring in place to indicate the quantity and type of competition expected within a market. However, effective LOE preparedness depends not just on competitive intelligence, but on translating that intelligence into insight. Understanding the implications of the competitive landscape is what enables meaningful strategic choices – data alone is insufficient.

Understanding Stakeholder Behaviors in Key Segments

While intra-molecular competition changes quickly post‑LOE, shifts in stakeholder behavior can be more subtle – though equally powerful – in shaping local market dynamics.

The role and influence of a priority stakeholder on final dispensing decisions may change with loss of exclusivity. The balance of power between prescribers, pharmacists, payers, and patients can change materially, but how this change manifests varies significantly by country. To understand the implications of this new environment there is a need to ask and answer the following questions:

- Who ultimately controls dispensing decisions post‑LOE?

- How motivated are stakeholders to influence dispensing outcomes – and what might the result be?

- What incentives (financial or structural) shape stakeholder behaviors?

While dispensing decisions are a key operating dynamic to consider, they can vary even within a single market. Therefore, it is important to also consider the number of distinct market segments that might exist. Distinct market segments – such as public vs. private, hospital vs. retail, or chain pharmacies vs. independent groups – may operate under different rules and incentives. Where these segments are large enough commercially – and different enough in terms of operating dynamics – they must be planned for separately on a local level.

In some cases, these distinct segments may create opportunities for sustained originator brand use post‑LOE, provided the value proposition is appropriately tailored to key decision makers.

Understanding Policy and Access Dynamics

Perhaps the most influential area that shapes local late lifecycle dynamics is the policy & access environment and how it evolves when a product loses exclusivity. There are three main areas of the policy and access environment to understand when planning for the impact of LOE in a given market.

Three dimensions are particularly critical to understand when assessing local LOE impact:

Pricing environment

Markets vary widely in how they regulate prices following loss of exclusivity. Some impose mandatory price cuts, regulated generic and/or brand discounts, or internal/external reference pricing – while others may allow free competitive dynamics to play out.

Cost‑management approach

Markets adopt different mechanisms to manage pharmaceutical expenditure and take advantage of the availability of low-cost generics. For example, some enforce generic use through access restrictions or mandatory price controls, while others rely primarily on a free competitive environment the primary driver of cost savings.

Generic usage policies

Mandatory substitution of brands for interchangeable generics, providing financial incentives for generic use, or financial penalties for missing generic usage quotas. can dramatically accelerate – or slow – brand erosion post-LOE.

Taken together, these policy and access factors tend to place markets into one of four broad late lifecycle archetypes.

1. Generic-dominant / Generic-favoring markets

These are markets where access policies enforce generic use as a driver of cost-savings following LOE, often through substitution mandates, strict usage quotas, or strong financial incentives.

2. Local brand-favoring markets

Markets where trust, relationships, and heritage drive preference toward local brands or local generics. Originator brands may retain relevance in specific niches, often within private sectors where brand loyalty persists.

3. Brand-/ generic-agnostic markets

Markets where price control (for both brand and generics) is the primary driver of cost saving, assuming that price reductions to maintain reimbursement or competitiveness with generics remains viable.

4. Originator brand-favoring markets

Markets where stakeholders have a strong preference for originator brands, and there is an open competitive environment that does not inhibit access to them. Local competitors may expand the size of the molecule’s market but have limited impact on the brand commercially as long as the value proposition is viable.

Navigating Loss of Exclusivity with Confidence

As we have illustrated, loss of exclusivity does not create a single, predictable outcome. Instead, it reveals a diverse and fragmented set of local realities that demand nuanced understanding and targeted strategic responses.

Without a clear framework for interpreting these dynamics, teams often experience uncertainty that cascades into misaligned planning, inconsistent execution, and missed opportunities to retain value.

Align Strategy specializes in supporting pharmaceutical teams as they prepare for and navigate loss of exclusivity. Our broad experience, proprietary frameworks, and deep understanding of local late lifecycle dynamics help teams move from decision-making uncertainty to confidence across diverse markets.

Explore our late lifecycle management programs and capabilities to learn more – or alternatively, read the next article in this series to see how we translate local market insights into actual planning: A Hybrid Archetyping Approach for Late Lifecycle Planning.

Discover our PSVA Framework, designed to help teams break lifecycle tactics down into four categories: product, solution, value, and asset. Our practical toolkit details what the PSVA framework is and why it’s useful with a closer look at the tactics available, alongside 10 late lifecycle case studies.